Join The Nomis Narratives

Latest Posts

Build vs. Buy: Why the Conversation has Changed

Ten years ago, the build versus buy conversation...Beyond Surface Yields: A Complete Framework for Auto Loan Profitability

The Experience Advantage After 20 years of...The Multibillion Wake-Up Call: Why Banks Must Evolve Beyond Basic A/B Testing

While banking executives debate IT budgets and...Building a Voice-Enabled Mortgage Assistant in Four Hours: A Lesson in Compound AI Systems

Most groundbreaking banking technology stories...Pricing Analytics, Deposits | May 1, 2025

When financial institutions turn to outside vendors or consultants for deposit analytics solutions, they’re often met with strategies that treat consumer and commercial deposits as two sides of the same coin. But this assumption reveals a critical gap in how vendors misunderstand and oversimplify the realities of commercial deposit management.

At Nomis, we’ve seen firsthand how these approaches often fail. We’ve seen claims like “price elasticity models work equally well for both segments” or “commercial industry verticals are just another analytic dimension.” These ideas might sound good on paper, but they don’t hold up in the real world.

We firmly believe we shouldn’t just be selling models; we’re expected to provide strategies rooted in real-life behaviors, relationships, and data. That’s why we say boldly: a one-size-fits-all approach doesn’t work in deposit analytics. Instead, banks need solutions that reflect the real-life complexities of their portfolios.

The Myth of a Unified Approach

Some analytics vendors promote the idea that their tools can seamlessly handle both consumer and commercial deposits using the same methodologies. This simply isn’t true. The reality? Consumer and commercial deposits differ dramatically in behavioral patterns and portfolio structure. Critical differences in relationship management, pricing dynamics, and market expectations make it essential to tailor your strategies. Treating the two segments interchangeably isn’t just inefficient; it can actively harm key client relationships.

Behavioral Differences Between Consumer and Commercial Deposits

Consumer deposits revolve around scale. Millions of accounts create extensive datasets that fuel predictive modeling. Segmentation, cohort-based pricing, and price-response models thrive here because of the consistency and predictability inherent in consumer behavior.

By contrast, commercial deposits operate in an entirely different landscape. These portfolios have fewer accounts with balances concentrated among a few critical clients. Each business has unique cash flow patterns, seasonality, and account needs. Averages and aggregate models fail in this space because the outliers dictate the portfolio’s performance. Successfully managing commercial deposits demands a granular, customized approach.

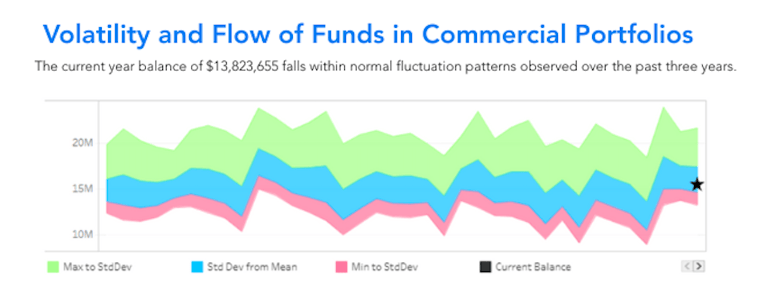

Volatility and Flow of Funds in Commercial Portfolios

One key challenge in commercial deposits is volatility. Business balances fluctuate due to factors like seasonal patterns, loan repayments, or liquidity events. This makes it tricky to distinguish between normal internal activity (e.g., paying down a loan at the same institution) and movement of funds to a competitor.

Misinterpreting this data can lead to serious missteps, such as unnecessary pricing adjustments or misaligned risk strategies. Platforms that lack the ability to analyze these critical flow-of-funds distinctions risk damaging client relationships or losing balances. The proper analytics can help banks pinpoint the root causes of balance changes, empowering smarter decision-making.

The Competitive Benchmarking Challenge

Another area where vendors misstep is commercial deposit benchmarking. Consumer deposit pricing is publicly available and segmented, allowing straightforward competitive analysis. Commercial deposit pricing, by contrast, is opaque and relationship dependent.

Without reliable competitor data, vendors must rely on internal benchmarks, which leaves significant analytical gaps. Predictive models built without this critical market context struggle to adapt when external conditions shift. This can be mitigated by pairing advanced analytics with banker expertise to create strategies that work even in the absence of publicly available comparisons.

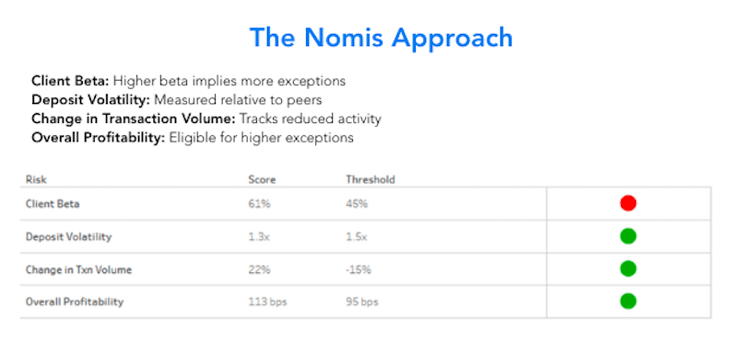

The Nomis Approach

Nomis’s approach is rooted in real-world expertise and guided by the unique challenges of commercial deposits. Here’s how we can help banks thrive in this space:

- Deep diagnostics: Identify what’s truly driving balance movement, whether it’s seasonality, pricing, or external competition.

- Exception pricing insight: Evaluate how custom pricing decisions impact profitability and align with customer lifetime value.

- Client-specific strategies: Develop tailored solutions that address the needs of your most important relationships.

- Risk thresholds: Distinguish between normal fluctuations and warning signs, empowering banks to act preemptively.

By combining these insights with advanced analytics, Nomis supports stronger, more effective portfolio management for commercial deposits.

The Takeaway: A Hybrid Future for Deposit Analytics

The idea that consumer and commercial deposits can share a single strategy is a myth that hurts both bank performance and client satisfaction. Consumer deposits demand optimization at scale based on vast datasets, while commercial deposits require relationship-focused, customized strategies that account for volatility and strategic nuance.

At Nomis, we’re building solutions that adapt to the complexities of both segments, leveraging the best analytics tools and decades of experience to guide banks through today’s challenges. Want to learn more about how Nomis can support your deposit strategies? Reach out today to see how we can help you build smarter, more data-informed decisions.

Get in touch at sales@nomissolutions.com or connect with us via nomissolutions.com to speak directly with our experts!

Written by: Ashwin Khanapur, Director of Product Management at Nomis Solutions