Join The Nomis Narratives

Latest Posts

Build vs. Buy: Why the Conversation has Changed

Ten years ago, the build versus buy conversation...Beyond Surface Yields: A Complete Framework for Auto Loan Profitability

The Experience Advantage After 20 years of...The Multibillion Wake-Up Call: Why Banks Must Evolve Beyond Basic A/B Testing

While banking executives debate IT budgets and...Building a Voice-Enabled Mortgage Assistant in Four Hours: A Lesson in Compound AI Systems

Most groundbreaking banking technology stories...Price Optimization, Pricing Analytics, Deposits | Sep 18, 2024

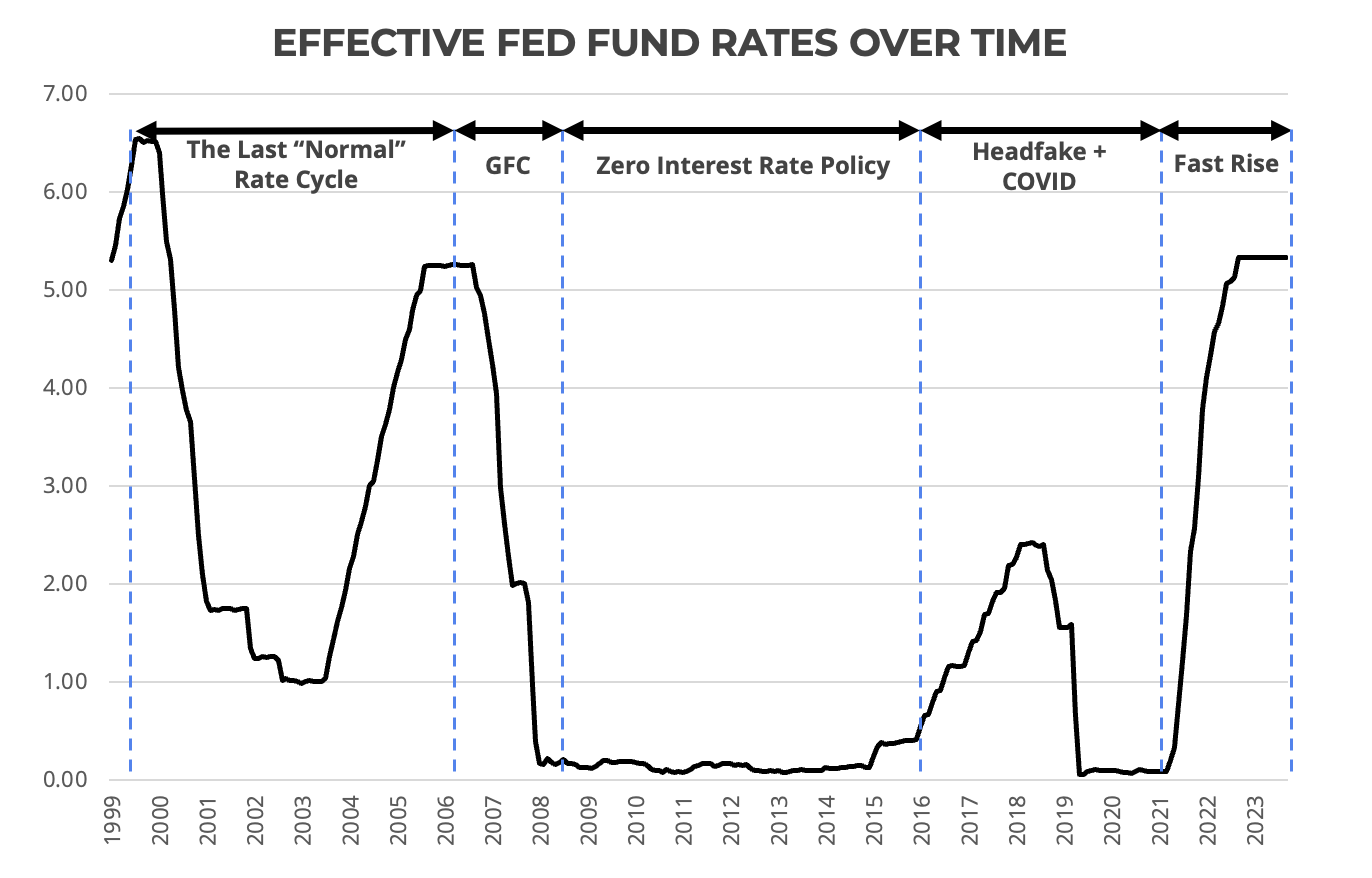

In the immediate aftermath of the Federal Reserve’s announcement of a 50 basis point rate cut at today’s FOMC meeting, we are entering uncharted territory for many financial institutions. This marks the first rate cut since the 2018 headfake and the first significant rate reduction since the 2008 financial crisis, and the implications for banks and credit unions, particularly in managing their deposit expenses, are profound.

At Nomis, we are dedicated to leading the charge in pricing science, and our latest research is focused on how banks and credit unions will navigate the challenges of managing deposit expenses in a falling rate environment. To shed light on this, the Nomis analytics team surveyed the largest 50 retail banks by assets, scrutinizing their public forward-looking statements concerning deposit expense expectations. Our team mined footnotes from 10-Qs, 10-Ks, earnings transcripts, and investor day presentations, particularly focusing on the 3Q and 4Q 2021 commentary—just before the recent rate hike cycle began.

Source: Federal Reserve Bank of St. Louis

Banks Historically Misjudged Deposit Costs During the Last Cycle of Rising Rates

Banks traditionally forecast deposit expense using a concept known as the deposit beta, which measures the sensitivity of deposit rates to changes in the federal funds rate. For example, a product with a 30% beta would see a 15 basis point rate change when the Fed Funds Rate moves by 50 basis points. However, these deposit beta assumptions are often closely guarded. Among the 50 banks we analyzed, only a subset disclosed their beta forecasts, with the weighted average expected deposit beta ranging between 20-30%. In reality, however, the actual deposit beta during this period was closer to 50-60%, a stark difference from the disclosed deposit beta forecasts.

Source: Beta estimates sourced from public sources including regulatory filings, investor presentations, and earnings transcripts in 3Q21 and 4Q21. Actual betas calculated using 3Q21 and 1Q24 filings. Results exclude Cullen/Frost, the only institution in our survey with a 2021 forecast beta higher than observed (50% forecast vs 43% realized).

This discrepancy is shocking: deposit expense grew twice as fast through the rising rate cycle as expected. Smaller banks experienced a 25-30% gap between projected and realized deposit beta, with larger banks doing marginally better with only a 20-25% delta. After 21 rate hikes in two years, being wrong by this much resulted in an eye-popping 75-110 bp NIM haircut.

The implications are equally significant and the economics are identical (but inverse) as rates fall. A deposit portfolio management team that is overconfident in its ability to achieve deposit beta targets may face an expensive falling rate cycle.

Strategic Considerations in Our New Era of Falling Rates

Given the expectation missteps that occurred during the rising rate cycle, Deposit Product Managers should carefully plan their strategy in these four key areas to avoid repeating the same mistakes and successfully navigate the new environment of falling rates.

1. Choosing To Be A First Mover or a Fast Follower

How quickly can and should your institution pass through rate reductions to its deposit portfolio? Will you lead the charge, even at the risk of alienating customers and triggering balance outflows, or will you opt for the potentially more costly strategy of waiting for competitors to lower deposit rates first?

To be able to answer this question, it's critical to have the foundational knowledge of how your specific deposit portfolio grows. Specifically, do you understand the balance between new-to-bank customers, growth in existing relationships, and the movement of money between different products? The real question is not just whether you’re ready to drop rates but whether you have a solid grasp on where your deposit growth is coming from and how your deposit portfolio reacts to pricing changes. Your ability to analyze these factors will determine whether you are well-positioned to make the call to lead or follow.

2. Managing Through CD and Promotional Bulges

In a falling rate environment, managing the impact of CD maturities and expiring promotional products is a critical challenge. Customers will compare current rates not only with market offerings but also with the rates they previously secured. This is particularly true for CDs and promotional MMDAs, where customers are more likely to shop around if the rate gap at renewal or promo expiry is too large.

From a price elasticity perspective, your portfolio’s price sensitivity is typically higher when rates first begin to fall, with an increased bias to attrition. If your institution has a large bulge of customers with maturing CDs or expiring promos, you must carefully balance reducing deposit expense with the risk of increased attrition.

If your retention models only consider contemporaneous price positioning and ignore acquisition rate, it's time to reevaluate your assumptions—quickly.

3. Identifying and Managing "Hot Money" Customers

Every institution has a unique mix of rate-sensitive and rate-insensitive customers, and the characteristics that drive these behaviors vary. In a falling rate environment, the optimal strategy is to aggressively reduce rates for rate-insensitive customers while maintaining competitive rates for rate-sensitive ones as long as possible. This is easier said than done. The key challenge is knowing who your rate-sensitive customers are and having the tools to act on that knowledge.

To execute this strategy effectively, you need to have the analytics to identify how different customer segments will respond to price changes and the system and marketing tools to target those segments effectively. Whether through direct mailers, online messaging, or product migration paths, the ability to guide customers through different behavioral pathways will allow institutions to maintain balance and minimize attrition, while achieving a blended portfolio rate reduction.

4: Leveraging Test-and-Learn

Over the past three years, banks have tested various strategies as rates have risen—from in-market rate adjustments to marketing campaigns and cash incentives. The best-performing institutions have been systematic in tracking the efficacy of these customer treatments, creating a robust library of strategies that they can deploy as needed. Whether the goal was to grow balances by a specific percentage or to extract a few extra basis points of net interest margin, these institutions have a well-documented playbook of successful approaches.

The institutions that have built this "test and learn" flywheel will have a significant advantage as rates begin to fall, armed with real data and proven strategies to inform their go-to-market approach. If your institution lacks this level of rigor, now is the time to start developing a "test and learn" system. Not many institutions have this kind of rigor, but the old adage applies: the best time to plant a tree was 20 years ago, and the second-best time is today. Without it, you risk consistently underperforming compared to what is possible.

In a landscape where interest rates are poised to fall, the strategies that banks and credit unions adopt today will define their success in the future. By learning from past missteps and leveraging advanced analytics, institutions can navigate this complex environment with confidence, optimizing deposit expenses while maintaining customer loyalty and portfolio stability. At Nomis, we provide advanced analytics solutions designed to empower banks and credit unions to make strategic deposit management decisions with confidence. To learn more, read our Optimizing Deposit Management: The Nomis Advantage flyer.

Note that the source for this information is premised on interest rate risk forecasting, typically a treasury exercise. In our experience, most institutions closely align their deposit treasury forecast expectations with their financial planning assumptions. If you believe your assumptions between product and treasury are materially different, give us a call—we’d be happy to discuss strategies to help unify them.

About the Author:

Wes West is the Chief Analytics Officer at Nomis Solutions, the foremost provider of end-to-end pricing analytics and execution technology. With a distinguished career at leading financial institutions, West brings unparalleled expertise and a track record of innovation to his role at Nomis. His extensive experience spans Retail, Strategy, Finance, and Treasury, offering unique insights into the world of financial analytics and strategic pricing. Connect with him on LinkedIn or reach out via email at wes.west@nomissolutions.com.