A Look at the Current Environment

The expectation that financial institutions will raise deposit rates in 2022 is based on a recovery and expansion scenario. However, circumstances in this rate cycle are unique from previous cycles. The amount of free cash currently held in depository institutions is unprecedented. In a normal rising-rate environment, one would expect to see depository institution rates moving in earnest after the Fed funds rate makes 100-150 basis points of movement. While the industry may see some upward rate movement from central banks in the medium term, the existing overabundance of funding and low loan demand, if exacerbated by a future bearish economy, could result in a lack of federally insured institutions making meaningful rate movement before central banks are forced to cut rates again.

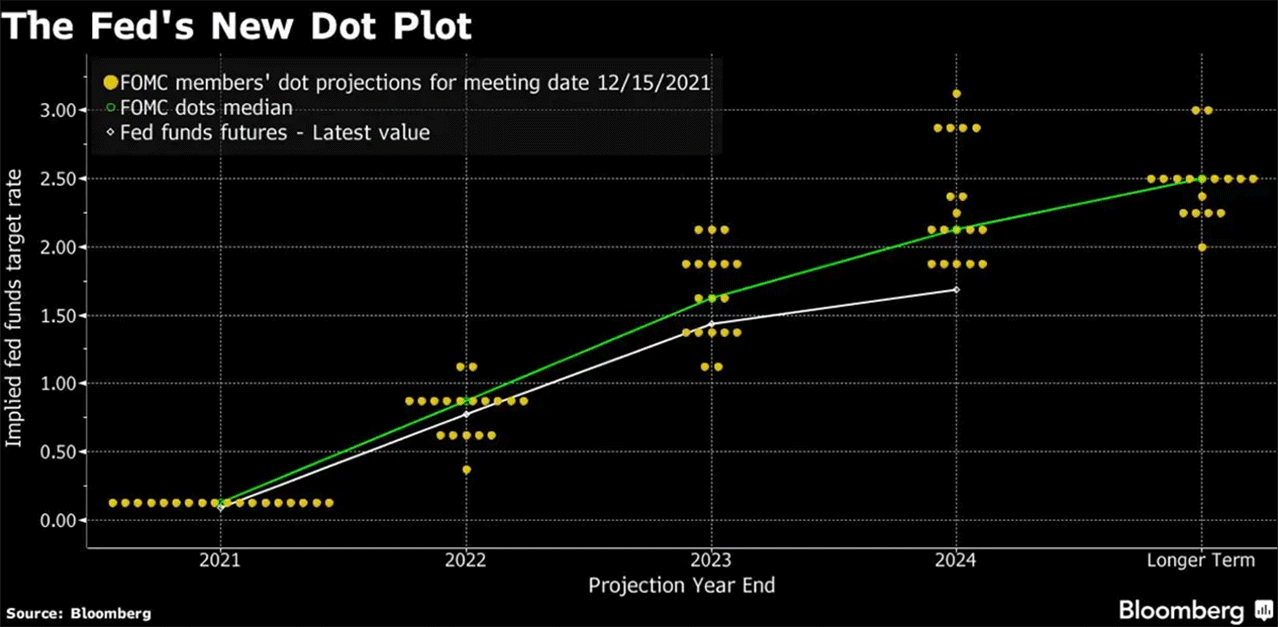

The “Dot Plot” exhibits strong consensus for rates to increase in 2022 by 75-100bps and will continue to rise until 2024 given current economic trends. Source: Bloomberg

So, what are financial institutions to do in light of limited opportunity to gain yield via margin expansion, especially while options for an expansion in fee income via punitive fees are restricted? Mortgage and wealth management fees are a popular strategic focus when margins are compressed, but these fees are sensitive to the rate cycle and the space continues to get more and more crowded by non-bank participants. It is also important to note that the necessity of expanding brand awareness and improving the digital experience has precipitated a wave of merger announcements over the past three years, and it is expected that this trend will continue as long as regulators permit. One must also be mindful of the persistent and somewhat urgent focus on deepening relationships and thus, achieving a greater share of wallet.

While this focus is nothing new, there has been an obvious shift and additional attention on leveraging robust technology and actionable data to better understand clients and specifically tailor pricing, rewards, and offers to their unique situation. Further, with fewer transactions taking place in the branch, banks are using technology and data to replace the contextualized service that was once provided by a smiling banker.

Banks that succeed in creating a rich and personalized experience will be able to gain a sufficient share of wallet and scale amid the ups and downs of rate cycles. The financial institutions that are too slow to adapt or are unable to allocate necessary resources to embrace this shift could find themselves as a good target for a merger or acquisition.